It has been a while since I have updated this blog. Doing a count of the posts I did in 2017, I have wrote about 8 posts for the year. Also, I have only did one post about Tianjin ZX this year. It is definitely low compared to the finance blogs I have been following this year! However, this blog is just a snapshot of my investment journey, only meant for the occasional passerby to browse through.

Personal Finances

In 2017, nothing monumental happened in my personal life. Compared to bloggers like kpo or bhalimking who have families or have a significant other, I am still operating life in 'Single Player' mode. In some ways, I think it simplifies my financial decisions. Career-wise, I made a big switch in industry jumping from Transport/Logistics to Finance/Investment. Although I often say that it is not as 'atas' as one may think, I definitely learnt a whole lot more in my new job. My new company puts out regular in-house research which I vehemently reads in my spare time and I hope will be able to reap some returns from them! Some people say to never do what you like in your job but I could not have disagreed more (ok, I think it is determined on a case-to-case basis).

For perhaps records purposes, my total net worth jumped 123.89% in the year of 2017. For what it is worth, this had been primarily attributed to my pay and much significantly less to my investments.

Investments

On to the main topic of this blog - 2017 reviews of my investments. First of all, the 2017 time-weighted return for STI ETF was 21.11%. Amazing one year return by all account. Sadly, this benchmark return blew past my portfolio time-weighted return which was a measly 5.38%.

This is the second year in running which I underperformed STI. This year of underperformance was really much bigger, a big loss attributed to SingPost. I felt that SingPost was really a good lesson about not falling in love with your stocks. For many years, I have told many people that SingPost was the crown jewel in my portfolio. At one point in history when Alibaba invested in it, SingPost traded double my purchase price. I remembered my dad asking me to consider divesting it. But I vividly remember thinking it could climb up to $3+ with the collaboration. It WAS possible, but the execution of investment was really poorly done. While I did analyze SingPost and saw its shortcomings many moons back, I did not really do anything. All said, I feel that the market is undervaluing SingPost currently and I will not be incline to sell it now (WHAT AM I DOING!).

This is the second year in running which I underperformed STI. This year of underperformance was really much bigger, a big loss attributed to SingPost. I felt that SingPost was really a good lesson about not falling in love with your stocks. For many years, I have told many people that SingPost was the crown jewel in my portfolio. At one point in history when Alibaba invested in it, SingPost traded double my purchase price. I remembered my dad asking me to consider divesting it. But I vividly remember thinking it could climb up to $3+ with the collaboration. It WAS possible, but the execution of investment was really poorly done. While I did analyze SingPost and saw its shortcomings many moons back, I did not really do anything. All said, I feel that the market is undervaluing SingPost currently and I will not be incline to sell it now (WHAT AM I DOING!).

Saving grace for my portfolio was really my investment in GLP. While I did not write a post about it here in my blog, it was really a conviction buy before I graduated in the year of 2016. While I bought at $1.95 based on my fair value calculation of $2.45, I held on to it through all the speculations and eventually to its delisting price of $3.38. Certainly adding this investment into my memorable trades. Those wild speculations and push-downs before announcement of winning bid gave me much entertainment in 2017. XIRR since purchase was 40.12%.

Another proud moment in 2017 was feeling the impact of my monthly investment in STI ETF with my siblings. First broached in 2016, our joint investment began in June 2016 and throughout 2017, we kept at it allowing us to enjoy the bull run. However, one reason why I will almost certainly underperform in 2017 was that I was buying at increasingly higher price.

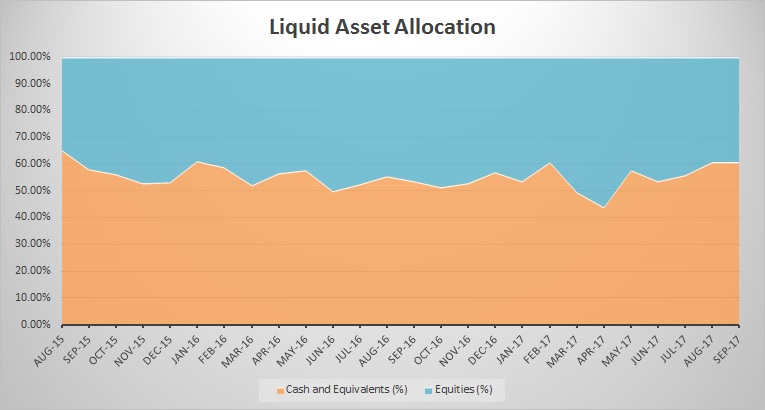

However, helping people other than myself make money is a very good feeling. In the current high of STI ETF, I am increasingly open to the idea of pausing our purchase and play with the idea of channeling the monthly investment into ABF Bond Index. I do not want to buy STI ETF at a high even though it is the essential of dollar-cost averaging because, our profits and holdings are already substantial. Channeling into ABF Bond Index hedges us against a market crash but I am apprehensive as my returns will be affected as US progressively hikes its interest rate. Time will see how I play around with this monthly investment of ours.

Dividend

Separately featured is my dividend received in 2017. In my 2016 Investing Report Card post, I stated my objective of receiving $1100 for 2017. Briefly mentioned in this post, I received $1083.87.

This is an increase of 13.84% over 2016. As pretty as it looks, this comes at a cost of increased capital deployment. The underlying capital increased by 61.30% as dividend yield dropped from 5.51% to 3.80%. The drop in yield was primarily due to me holding less REITs or Trusts. In addition, SingPost stopped its high dividend payout.

2018 Outlook

Based on research and outlook, 2018 looks like a continuation of 2017 although at a muted pace. Given this, I will look to enhance my alpha through riskier investment balanced by re-allocating my GLP capital into ABF Bond Index. In particular, I will be paying more attention into natural resources like oil and commodities as inflation in US may be coming into play in 2018 and potentially throwing a wench into the bull run.

Hopefully in 2018, I can have enough time, interest and energy to push out a few stocks write-ups. All the best to your investing journey in 2018.

Thank you for reading!